36 / 40

36 / 40

36

Better Pork

October 2016

MOE’S

MARKET

MINUTE

W

ill there be more pork on

the menu in 2017? USDA’s

(United States Department

of Agriculture) latest demand and

supply estimates point to a year-on-

year increase in U.S. pork demand

of 557 million pounds for 2017. U.S.

pork production, though, is expected

to outscore demand and rise by 603

million pounds next year. Pork seems

to have been replacing beef on the

dining table due to lower prices.

USDA forecasts U.S. hog pro-

duction to hit record highs in 2016,

and multi-month lows in wholesale

pork prices suggest that grocers are

struggling to sell the pork already

on hand and adjust to the reality of

big hog numbers. The key June 2016

Hogs & Pigs report showed U.S. hogs

inventory had expanded more than

expected and has since been weigh-

ing on prices.

U.S. inventory of all hogs and

pigs on June 1, 2016 was 68.4 mil-

lion head, up two per cent from June

1, 2015. This is the highest June 1

inventory of all hogs and pigs since

estimates began in 1964. Breeding in-

ventory, at 5.98 million head, was up

one per cent from last year. Market

hog inventory, at 62.4 million head,

was up two per cent from last year.

This is the highest June 1 market hog

inventory since estimates began in

1964.

The Canadian hog herd, com-

pared to July 1, 2015, was up 1.9 per

cent (at 13.5 million head) at mid-

2016. The breeding herd was up one

per cent (at 1.24 million head) and

market hog inventory was up two per

cent (at 12.2 million head). The Ca-

nadian hog herd is 20 per cent of the

size of the U.S. herd. Canada is the

source for about three-fourths of U.S.

pork imports plus about six million

live hog imports each year.

After seeing steep price rises dur-

ing the initial half of 2016, lean hog

futures fell below $60 per pound

in August as investors continued

liquidating their long (buy) positions.

U.S. Commodity Futures Trading

Commission (CFTC) data shows that

speculative managed money funds

have been reducing their net long

position (buying exposure) since late

June due to plentiful supplies.

Lean hogs – net speculative managed

money positions

According to U.S. Meat Export

Federation, which based its calcu-

lations on USDA data, U.S. pork

export volume was up two per cent

to 1.1 million tons for the first half

of the year but value was down four

per cent to $2.77 billion. Exports to

China/Hong Kong finished the first

half of 2016 at 80 per cent higher

than a year ago in volume (284,900

tons) and 63 per cent higher in value

($540.5 million). Rabobank estimates

China will see a supply gap of two

million tons in 2016 owing to floods

and production issues. The country

will likely maintain a similar level of

imports even when local production

recovers in 2017.

Due to China’s pork prices being

nearly twice that of competing coun-

tries, pork imports are going strong.

The European Union, though, is the

main exporter of pork and variety

meat to China. Although the United

States has increased its pork exports

to China, the lack of eligible U.S.

pork production plants has hindered

the United States from capturing

more of the market.

Canada looks most likely to

increase its trade with China as it

has one of the largest supplies of

ractopamine-free pork. The decline

in the value of the Canadian dollar is

another advantage. Though

Chinese import prospects are a

strong boost for U.S. and Canadian

pork exports, it is important to rec-

ognize the swings in Chinese demand

and realize that growth in other key

markets is essential.

USDA forecasts 2016/17 will pro-

duce the United States’ first 15-bil-

lion-bushel corn harvest and the first

four-billion-bushel soybean harvest.

These record harvests will help lower

feed costs as we go into 2017. This

decline is not likely to be sufficient to

keep hog profits up, as it doesn’t do

much to boost hog prices. Demand

and exports will have to tick up to

boost hog prices.

Swine dining in 2017

Pork demand is expected to rise in 2017 and so is production.

by MOE AGOSTINO and ABHINESH GOPAL

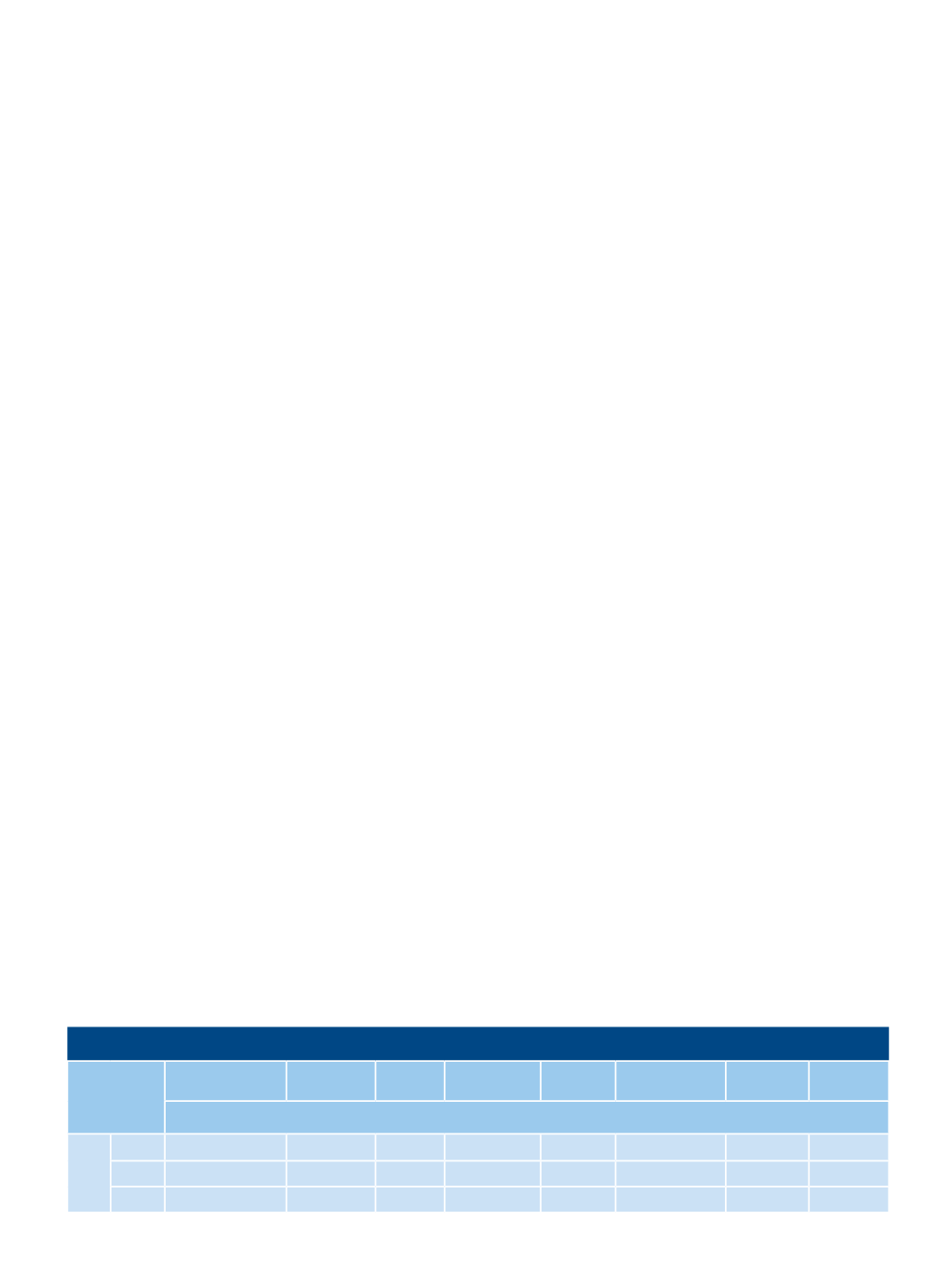

U.S. Pork Supply and Use

Item

Beginning Stocks Production Imports Total Supply Exports Ending Stocks Total Use Per Capita

Million Pounds

Pork

2015

559

24,517

1,111

26,187

4,941

590

20,656

49.8

2016

590

24,923

1,150

26,662

5,218

625

20,819

49.8

2017

625

25,526

1,160

27,311

5,300

635

21,376

50.8

Source: USDA